The DEA's expedited administrative hearing on cannabis rescheduling, which began June 29, 2026, with a mid-July target for completion, has handed investors a concrete calendar date to rally around. The AdvisorShares Pure US Cannabis ETF (NYSEARCA: MSOS) has risen 99.2% over the trailing year - almost entirely on that hope. Yet it still trades 81.0% below its September 2020 launch price. The gap between those two numbers is the whole story.

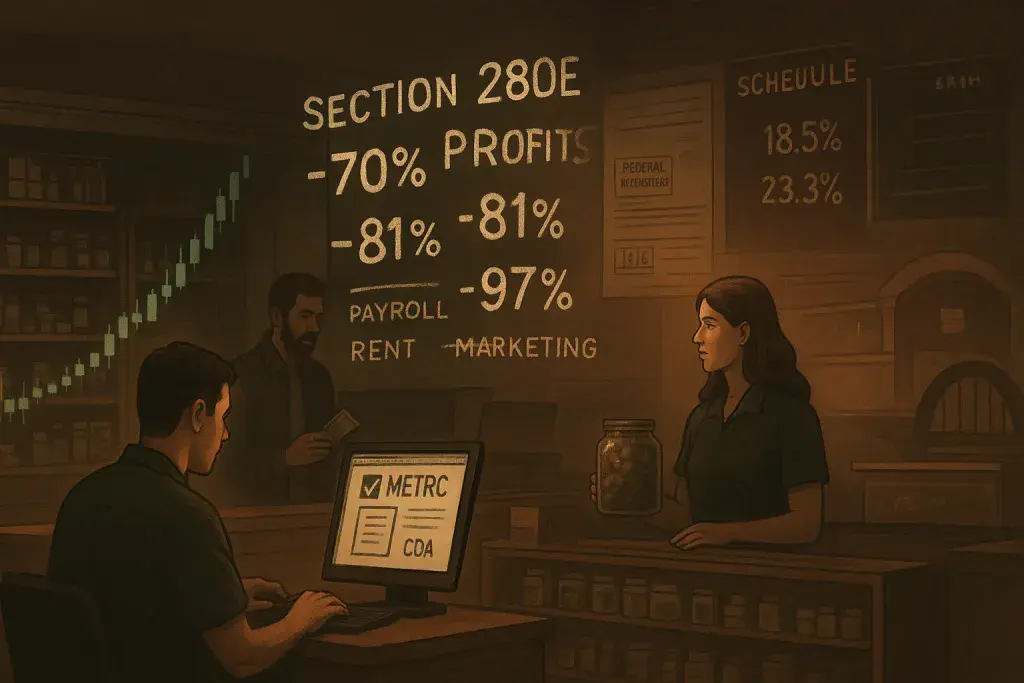

For licensed operators - multi-state operators with dozens of dispensary locations, independent retailers running a single budroom, and the technology vendors who serve them - what matters is not the stock price. What matters is whether Section 280E of the federal tax code finally gets cleared off the books. Right now, cannabis sellers cannot deduct ordinary business expenses: payroll, rent, marketing, compliance software, point-of-sale systems. They are taxed on gross profit rather than net income, pushing effective federal tax rates well above 70% for many U.S. operators. That single structural burden has done more damage to dispensary economics than any state excise tax or license cap. Operators working through sophisticated platforms - providers of cannabis POS for Nevada dispensaries, for instance - understand better than most that the technology to run a compliant, efficient retail operation exists; the tax code is what makes profitability genuinely difficult.

A move from Schedule I to Schedule III would remove 280E's reach over cannabis businesses. That is the actual mechanism driving investor enthusiasm. A final rule published in the Federal Register following the DEA hearing would, in theory, give multi-state operators access to the same ordinary deduction structure that a liquor retailer or a pharmacy takes for granted. The operational implications would be immediate: lower effective tax bills, more cash available for inventory, compliance infrastructure, and debt service. For operators who have been cannibalizing working capital to cover tax obligations, it would represent genuine structural relief.

The Prediction Markets Are Not Impressed

Here's the catch. The traders pricing contracts on Polymarket - people putting actual money behind their convictions - are not buying the bull case. The contract on rescheduling by the end of July implies an 18.5% probability. The year-end contract sits at 23.3%, and it has fallen nearly 10 cents over the past week. A prior contract resolving on rescheduling by March 31 closed at zero. That is not a cohort of pessimists being contrarian. That is a market reflecting a consistent pattern of federal cannabis reform stalling after generating enormous price momentum.

The rhyme with prior cycles is almost uncomfortable to catalog. The 2018 Canadian legalization wave sent Tilray Brands (NASDAQ: TLRY) above $223 on a split-adjusted basis. SAFE Banking legislation cycled through Congress starting in 2019 and died in the Senate repeatedly. The 2021 post-election rally faded without legislative resolution. The 2024 DEA rescheduling proposal - the direct predecessor to this current proceeding - disappeared into administrative limbo. Canopy Growth (NASDAQ: CGC), which crested above $241 in mid-2021, now trades at roughly $0.99, a 99.6% drawdown over five years. Tilray has shed 97.5% on the same timeline. The pattern of euphoria followed by collapse is not a bug in this trade; at this point, it is essentially the defining feature.

What Operators Should Actually Be Watching

For dispensary owners and multi-state operators, the rescheduling calendar is worth monitoring - but it should not drive operational strategy. The businesses that survived the 2021 run-up and the subsequent capital drought did so by controlling what they could control: inventory management, wholesale pricing discipline, compliance documentation, and cost structure. Those fundamentals do not change based on what the Federal Register publishes.

If Schedule III does clear - and it remains a genuine possibility, probability markets notwithstanding - the operational benefit flows through the tax line, not through any change to state-level licensing, seed-to-sale tracking requirements, COA obligations, or compliant packaging mandates. State regulatory frameworks stay intact. METRC integrations stay intact. Age-verification protocols stay intact. Rescheduling does not simplify the compliance stack; it changes one federal tax calculation. Operators should plan accordingly rather than treating it as a reset button on the entire regulatory burden they carry.

To put it plainly: if rescheduling happens, it is a meaningful financial improvement for licensed businesses already generating revenue. It does not create a new market, dissolve existing compliance costs, or resolve the banking constraints that continue to force many dispensaries into cash-heavy operations. SAFE Banking, which would address the payments infrastructure problem, remains a separate legislative ask - and its own track record in Congress is well documented. One reform does not deliver the other.

The Risk of Pricing the Outcome Before It Arrives

The 99.2% MSOS run reflects the market pricing in a meaningful probability of a favorable outcome. If the DEA hearing concludes without a clear path to a final rule, or if the rule faces successful legal challenge - a real possibility given the administrative record - that embedded optimism has nowhere to go but out. For ancillary businesses whose valuation or revenue projections have been tied to the rescheduling narrative, that unwinding creates its own operational risk: tighter vendor credit, reduced capital availability, and slower technology adoption cycles across the retail tier.

What's striking here is that none of this is new information. The cannabis industry has rehearsed this particular sequence of events multiple times. The businesses that will be positioned well on the other side of the current cycle are the ones treating the DEA hearing as a contingency rather than a certainty - running lean compliance operations, maintaining accurate inventory records, and managing cash carefully regardless of what the Federal Register does or does not say before year-end.