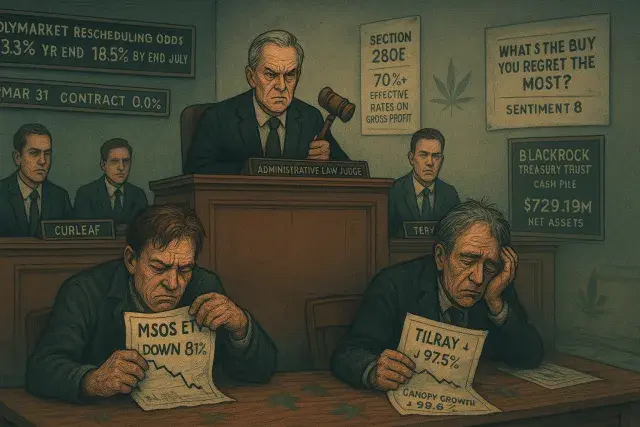

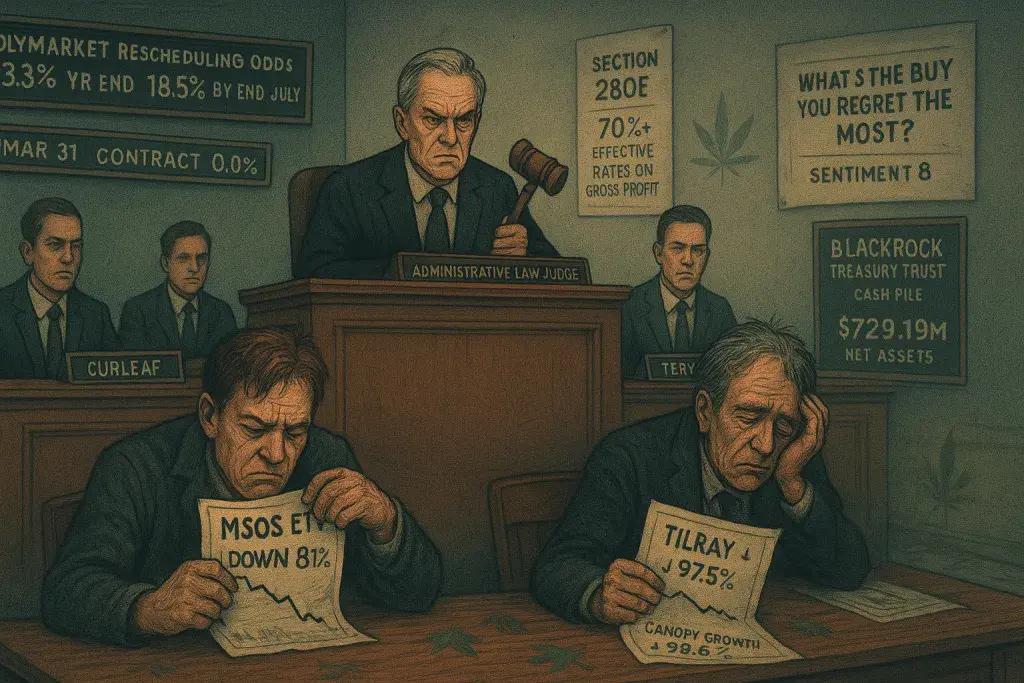

The DEA's expedited administrative hearing on Schedule III rescheduling, which began June 29, 2026, represents the most concrete regulatory movement the U.S. cannabis industry has seen in years. Prediction markets, however, are not celebrating. The Polymarket contract on rescheduling by year-end prints 23.3% - and it fell nearly 10 cents in a single week. That gap between headline momentum and market conviction is exactly where cannabis investors have lost money before, repeatedly, and at scale.

The structural stakes this time are real in a way that earlier rallies were not. Section 280E of the tax code - the provision that strips cannabis businesses of standard business deductions because they sell a Schedule I controlled substance - has been quietly bankrupting otherwise viable operators for years. Dispensaries and multi-state operators cannot deduct rent, payroll, or marketing against their federal taxable income the way any other retailer can. The result is effective federal tax rates that can exceed 70% on gross profit, not net income. Operators running competent retail businesses, with trained staff, POS software for Maine cannabis retailers and compliant seed-to-sale tracking in place, have still faced tax bills that would make a conventional small-business owner physically ill. Schedule III rescheduling removes the 280E burden. That is the unlock the AdvisorShares Pure US Cannabis ETF - MSOS - has priced in with a 99.2% trailing-year gain.

Here's the catch: MSOS still trades 81.0% below its September 2020 launch price. The ETF's largest position, Curaleaf, represents 12% of net assets. TerrAscend sits at 3%. The fund carries $729.19 million in net assets and a 7% cash position held in BlackRock Treasury Trust - a defensive posture that tells its own story. Beneath the equity-price enthusiasm, the operator economics are punishing. These are not businesses temporarily depressed by sentiment. They are businesses structurally disadvantaged by a tax code provision that no other licensed retail category faces.

History Does Not Flatter the Optimists

Cannabis investors have stood at this intersection before. The 2018 Canadian legalization wave pushed Tilray Brands above $223 on a split-adjusted basis. SAFE Banking legislation moved through the House repeatedly starting in 2019 and stalled in the Senate each time. A post-election rally in 2021 faded. The 2024 DEA rescheduling proposal - the direct predecessor to the current hearing - dissolved into administrative limbo. Canopy Growth crested above $241 in mid-2021 and now trades near $0.99, a 99.6% drawdown. Tilray has shed roughly 97.5% over the same five-year span.

What makes those numbers particularly instructive is the structural quirk embedded in them. Tilray and Canopy are Canadian licensed producers. They are not subject to 280E. They do not operate U.S. dispensaries. Their effective tax treatment bears no resemblance to the MSOs the rescheduling conversation is actually about. Yet their share prices tracked U.S. reform sentiment for the better part of a decade as though they did. Tilray's fiscal third-quarter net loss came in at $25.23 million on $206.73 million in revenue. Canopy's most recent quarter showed $71.25 million in revenue against a net loss of $154.72 million, with an accumulated deficit of C$11 billion. These are not numbers that reflect reform optimism. They reflect businesses that consumed enormous capital during the rally years and are now working through the consequences.

What a Final Rule Would Actually Mean for Operators

For the U.S. operators inside MSOS, 280E relief is not a political symbol. It is a cash-flow event. Deductions currently unavailable - cost of goods sold adjustments, facility costs, employee benefits - would land on the income statement. Effective tax rates would compress toward conventional retail ranges. MSOs currently raising capital at steep discounts, because lenders and equity investors apply a structural-disadvantage haircut to cannabis balance sheets, would see that discount narrow. Valuations built against gross profit rather than net income would reset against something closer to actual earnings.

The math, in isolation, is straightforward. The timing is not. The hearing conclusion is targeted for mid-July, with a potential final rule in the Federal Register to follow. That sequence involves a DEA administrative law judge, a formal rulemaking process, and a Department of Justice sign-off. None of those steps are guaranteed, and the prediction-market tape - with year-end rescheduling at 23.3% and end-of-July at 18.5% - reflects exactly that uncertainty. A prior contract resolving on rescheduling by March 31 closed at zero.

The Retail Sentiment Divide That Should Give Everyone Pause

Retail investor behavior in this cycle mirrors the pattern precisely. WallStreetBets posts in early June carried sentiment scores of 90 tied to MSO uplisting catalysts, with at least one trader documenting a $2.1 million MSOS position. Meanwhile, Tilray's most recent tracked Reddit thread - titled "What's the buy you regret the most?" - carried a sentiment score of 8. Euphoria and exhaustion, same forum, same week.

To put it plainly: rescheduling will likely occur at some point. 280E is an anachronism that survives only because federal cannabis reform moves slowly and the political will to accelerate it has proven unreliable. When a final rule does appear in the Federal Register, U.S. cannabis operators will face a fundamentally different cost structure, and the capital markets will reprice accordingly. The problem is that the market has already priced that outcome multiple times - in 2018, in 2021, in 2024, and again now - and each false dawn left the next entry point lower. Tilray carries an analyst target of $9.66, well above its current price. Canopy's target of $1.22 sits only marginally above where it trades today. Neither figure suggests that Wall Street expects a near-term resolution to close the gap. The hearing is on the calendar. The structural case is real. History suggests those two facts are not the same thing.