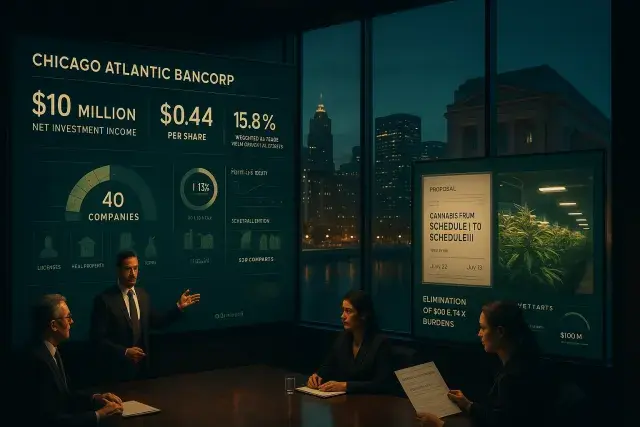

Chicago Atlantic BDC, the only publicly listed business development company focused primarily on cannabis industry lending, reported record net investment income of $10 million - or $0.44 per share - for the first quarter of 2026, the company disclosed during its earnings call on May 14. The results arrived against a backdrop of meaningful federal policy movement, with the Department of Justice formally announcing a proposal to move state-licensed medical cannabis from Schedule I to Schedule III classification. For cannabis operators and their lenders alike, the timing is significant.

The BDC's portfolio now spans 40 companies, with roughly 24% of invested capital going to non-cannabis businesses across multiple sectors. For cannabis operators thinking through their own capital structures, the context matters: private credit from specialty lenders like Chicago Atlantic has been, for years, one of the only reliable debt financing channels available to licensed cannabis businesses locked out of conventional banking. That structural reality - rooted in 280E tax exposure, federal illegality, and institutional lender aversion - is why firms like Chicago Atlantic command a weighted average yield on debt investments of 15.8%, compared to 10.8% for the average public BDC. Operators and investors tracking the financing side of this industry, whether evaluating debt terms or building out technology infrastructure like cannabis pos software oregon markets have increasingly demanded, understand that the cost of capital in cannabis rarely resembles other regulated industries.

The rescheduling announcement carries direct financial implications for licensed operators. The elimination of 280E - the tax code provision that currently bars cannabis businesses from deducting ordinary business expenses because they traffic in a federally controlled Schedule I substance - would allow medical cannabis operators to be taxed on pretax income rather than gross profit. That distinction is enormous. A dispensary with strong gross revenue but heavy payroll, rent, and compliance costs currently pays taxes on revenue figures that bear no resemblance to actual business profit. Post-rescheduling, those operators would finally receive the same tax treatment as virtually every other retail business in the country. Chicago Atlantic's management was careful to note that impact will vary by operator depending on medical market exposure - fair enough, since many multi-state operators have mixed adult-use and medical revenue streams, and recreational cannabis was not included in the initial rescheduling announcement.

What the Rescheduling Timeline Actually Means for Operators

An administrative hearing scheduled for June 29 will consider rescheduling for recreational cannabis, with a conclusion expected by July 15. The outcome of that hearing - not a certainty - could expand 280E relief beyond medical-only operations. Chicago Atlantic's management flagged that a favorable result could accelerate capital markets activity and M&A in the broader cannabis sector. That's a reasonable read. Historically, M&A in cannabis has been constrained not just by capital scarcity but by the complexity of state-by-state licensing transfers, regulatory approval timelines, and the simple fact that distressed sellers often can't command valuations that make deals pencil out. Remove 280E from the equation for adult-use operators, and the balance sheet math changes. Buyers with access to private credit or public markets may move more aggressively.

Still, Chicago Atlantic was direct about its own underwriting discipline: the company stated it will maintain its standards based on today's regulatory framework, not anticipated future reform. That's the correct posture. Federal policy on cannabis has a long history of moving slowly, reversing, or stalling entirely. Operators who have structured their business models around expected regulatory outcomes - rather than current operating realities - have repeatedly been caught out.

Portfolio Construction and What It Signals for the Lending Market

A few specifics from the quarter are worth examining. Chicago Atlantic funded $93.9 million across seven portfolio companies, including three new borrowers. The company reported zero nonaccruals - none of its loans are in default status - against an industry BDC average of 3.4% of cost in nonaccrual positions. The debt-to-equity ratio sits at 0.18x, well below the BDC industry average of 1.3x, which the company itself flagged as room to grow the portfolio further without exceeding standard leverage thresholds. The credit facility stands at $100 million, with approximately $50 million in remaining borrowing capacity as of mid-May.

The 100% senior secured debt structure is also notable. Other BDCs carry an average of roughly 25.5% of their portfolios in subordinated debt, equity, or joint ventures - exposure categories that tend to behave poorly when credit conditions tighten. Senior secured positions, by contrast, carry first-lien priority against borrower assets, which in cannabis operations typically include licenses, real property, inventory, and cash. For cannabis operators, that means lenders at this level expect - and take - real collateral. The days of unsecured or loosely documented cannabis debt have largely passed for institutional lenders operating in this space.

The Broader Implication for Cannabis Operators Seeking Capital

What this earnings report communicates to the broader cannabis industry isn't subtle. The specialty lending market for cannabis remains narrow, yields remain elevated, and competition from conventional lenders hasn't materialized at scale - in part because federal illegality persists, and in part because the compliance complexity of cannabis lending requires sector-specific expertise most bank credit teams simply don't have. Chicago Atlantic's management noted that ongoing federal constraints and industry complexity should limit new large-scale lending competition in the near term. That assessment is consistent with current market conditions.

For dispensary operators and multi-state operators evaluating debt financing, the practical takeaway is this: access to capital in cannabis is improving at the margins, not by transformation. Rescheduling, if it proceeds for both medical and recreational cannabis, will strengthen operator balance sheets and improve debt serviceability over time. But the fundamental structure of the lending market - high yields, senior secured terms, specialist lenders - won't dissolve overnight. Operators who have built financially disciplined businesses, with clean compliance records, accurate seed-to-sale tracking, and defensible margins, will be better positioned to access credit on improving terms. Those who haven't done that work will find the lending market still unforgiving, regardless of what happens in Washington.